Blue Sky Filing Deadlines

Category: Blue Sky Filing Deadlines

Raising capital in the United States often requires more than just federal compliance. While many companies focus on SEC filings such as Form D, state-level requirements under Blue Sky laws still apply whenever investors are located in different jurisdictions.

The challenge is not understanding that filings are required. The challenge is tracking what needs to be filed, where, and when across multiple states. Missing even one requirement can lead to penalties, delays, or additional filings.

This guide focuses on one thing: a clear and practical Blue Sky filing checklist you can use to stay organized and avoid common compliance mistakes.

Blue Sky Filing Checklist

Blue Sky compliance works best when approached as a structured process rather than a last-minute task. Breaking the process into stages helps ensure that nothing is overlooked, especially when dealing with multiple states and filing requirements. Below is a simplified checklist that companies use to manage Blue Sky filings from preparation through submission and ongoing compliance.Pre-Filing Checklist

Before any state filings are submitted, companies need to confirm that the offering structure and documentation are aligned with both federal and state requirements. This preparation stage is where most compliance issues can be prevented. A typical pre-filing checklist includes the following steps:- Confirm the federal exemption being used, such as Regulation D, Regulation A, or Regulation Crowdfunding

- Submit Form D with the SEC when required

- Identify all states where investors are located

- Review state-specific notice filing requirements for each jurisdiction

- Prepare offering documents and disclosures

- Verify investor residency information

State Filing Checklist

Once preparation is complete, the next step is to submit the required filings to each applicable state. This stage requires careful coordination, as each jurisdiction may have different procedures and fee structures. Companies typically complete the following actions during the filing stage:- EDGAR setup: File the Form ID application with the SEC and create the EDGAR account (depending on SEC timeframes, this can take 1–2 weeks).

- Offering documents: Finalize the PPM and other offering materials, including the subscription agreement.

- Subscription workflow: Ensure the subscription process is fully set up, including document signing, escrow arrangements, and payment collection/processing.

- Investor roster and sales tracking: Prepare and maintain an investor roster, and track investors and sales by state (including first sale dates and amounts) to ensure deadlines aren’t missed (often within 15 days after the first sale for many notice filings).

- State filing requirements: Determine the state-specific requirements and prepare filings**

- State notice filings: Submit state filings and fees, and record confirmations**

Post-Filing Checklist

After the initial filings are submitted, compliance responsibilities continue. Changes in the offering or investor base can create new filing obligations that must be addressed promptly. To maintain compliance, companies will need to monitor the following:- Sales to investors in new states

- File amendments if offering details change

- Answer state regulator inquiries and deficiency requests

- File annual renewals before the 12-month mark to the SEC and states

- Maintain records of all filings and confirmations

A Simple Checklist Prevents Costly Issues

Blue Sky filings are not inherently complicated, but they require attention to detail and consistent tracking across multiple jurisdictions. Without a structured process, it becomes easy to miss deadlines or overlook state-specific requirements. A clear checklist allows companies to stay organized, reduce administrative errors, and maintain compliance throughout the offering process. For companies managing multi-state offerings, having a reliable filing process in place is often the difference between smooth compliance and costly delays.

Raising capital under Regulation D or another federal exemption often feels straightforward once the SEC filing is complete. But many issuers learn the hard way that state compliance is where small procedural errors turn into formal notices from regulators. A Blue Sky deficiency letter can interrupt your offering, create unnecessary legal expense, and raise avoidable questions about your compliance controls.

Most deficiency letters are not issued due to fraud. They are triggered by preventable mistakes. Understanding the patterns behind these errors is the first step toward avoiding them.

The difference between smooth compliance and regulatory correspondence is often just a few days.

What Is a Blue Sky Deficiency Letter?

A Blue Sky deficiency letter is a formal communication from a state securities regulator identifying a problem with your notice filing, timing, documentation, or compliance posture. It is typically issued when a regulator believes your filing is incomplete, late, inaccurate, or inconsistent with state requirements. In many cases, the regulator will request corrective action within a defined timeframe. In more serious cases, the deficiency may escalate into late fees, administrative penalties, or even a temporary suspension of offering activity in that state. A deficiency letter is a warning sign. It is not yet enforcement, but it signals regulatory attention. Responding quickly and accurately matters, which Blue Sky Comply can help with. But preventing the letter altogether is far better.Mistake #1: Assuming Federal Exemption Eliminates State Obligations

One of the most common triggers of deficiency letters is the assumption that a federal exemption solves everything. Issuers often rely on Rule 506 under Regulation D and believe that because the offering is federally exempt from registration, no additional state action is required. While Rule 506 offerings are considered covered securities and are preempted from state registration, they are not exempt from state notice filing requirements. States still require:- A copy of Form D

- Payment of the required state filing fee

- Consent to service of process

Mistake #2: Missing the 15 Day Filing Deadline

Timing is one of the most frequent causes of deficiencies. Most states require that a Blue Sky notice filing be made either before the first sale in the state or within 15 calendar days after the first sale. The problem arises when companies accept investor funds and only later confirm which states require filing. Once the 15-day window has passed, the filing is considered late even if it is eventually submitted. Late filings can trigger:- Monetary late fees

- Administrative penalties

- Unregistered sale designation and penalty

- Formal deficiency notices

| Scenario | Filing Timing | Regulatory Outcome |

| Notice filed before first sale | Pre-filing compliance | No deficiency |

| Notice filed within 15 days | Timely compliance | No deficiency |

| Notice filed after 15 days | Late filing | Deficiency letter likely and possibly late fees |

| No filing submitted | Ongoing violation | Enforcement risk |

Mistake #3: Accepting Investors From States Where No Filing Exists

Blue Sky obligations are triggered by the investor's residency, not the issuer's location. An issuer may be headquartered in Texas, but if an investor resides in California, New York, or Illinois, a filing is required in that investor’s state. Online capital raises make this even more complex because investors can participate from anywhere. A common error occurs when:- An investor commits funds from a state where no notice has been filed

- The company processes the investment before completing the state filing

- The filing is rushed after the fact

Mistake #4: Incomplete or Incorrect State Filings

Not all deficiencies are about timing. Many involve documentation errors. State filings often require more than simply uploading Form D. Common administrative mistakes include:- Incorrect fee amount

- Missing correct state-specific forms

- Incorrectly completed filings and forms

- Filing in the wrong system

- Omitting other requirements

Mistake #5: Improper General Solicitation in Rule 506(b) Offerings

Marketing conduct can also trigger Blue Sky scrutiny. Rule 506(b) prohibits general solicitation and advertising. While this is a federal rule, states also enforce anti-fraud and solicitation restrictions under their Blue Sky statutes. Examples that create problems include:- Public social media posts promoting the offering

- Open demo day presentations

- Broad email campaigns without pre-existing relationships

Mistake #6: Failing to File Amendments or Annual Renewals

Compliance does not end after the initial filing. Certain states require annual renewal filings if the offering remains open for more than 12 months. Others require amendments if there are material changes to the offering. Detailed guidance on what constitutes a material change and when updates are required can be found in our Form D Amendment Triggers Explained guide. Issuers sometimes forget that these events automatically trigger updated filings at both the SEC and state level. A regulator who notices outdated information may issue a deficiency letter requesting correction. Ongoing compliance requires structured calendar management, not just initial submission.The True Cost of a Deficiency Letter

While a deficiency letter may seem procedural, the consequences can extend beyond administrative correction. Potential impacts include:- Late fees that range from hundreds to thousands of dollars

- Legal fees for response and remediation

- Enforcement action, including prior offering rescission in the state, a temporary ban from doing offerings in the state, and civil legal judgments

- Reputational concerns with future regulators

How to Prevent Blue Sky Filing Deficiencies

Preventing deficiency letters requires a structured approach. While each offering differs, effective compliance programs typically include the following elements:- Conducting a state-by-state analysis before launch

- Identifying potential investor states during marketing planning

- Filing proactively where marketing is expected

- Implementing investor residency screening during onboarding

- Maintaining a centralized compliance calendar

- Monitoring amendment triggers

Building a Sustainable Blue Sky Compliance Framework

Blue Sky compliance becomes more complex as offerings expand across multiple states. What begins as a single Form D filing quickly turns into multiple state filings. A sustainable compliance framework includes:- Clear assignment of responsibility within the organization

- Standardized documentation processes

- Regular internal compliance reviews

- Coordination between legal, finance, and investor relations teams

Precision Prevents Problems

State regulators are not looking for perfection, but they do expect precision. Most Blue Sky deficiency letters stem from inadequate legal support. Blue Sky Comply’s team of experts works with state regulators on a regular-basis and knows each of them well, which helps prevent such compliance issues discussed in this article. By tracking investor sales carefully and maintaining proper compliance, issuers can avoid unnecessary regulatory scrutiny.

If you’re raising private capital in the U.S., there’s a good chance you’re relying on Regulation D. That’s where SEC Form D comes in, a short notice filing for private offerings conducted by any companies in the United States - yes, this means all companies in the US who sell securities to investors must file a Form D to the SEC with the accompanying Blue Sky filings.

The SEC Form D doesn’t get you “approval,” but it does provide basic disclosure of key details of your exempt offering and starts the 15-day filing window for your state-level “blue sky” obligations. In other words, it’s a notice form with consequences for compliance, investor confidence, and your fundraising momentum.

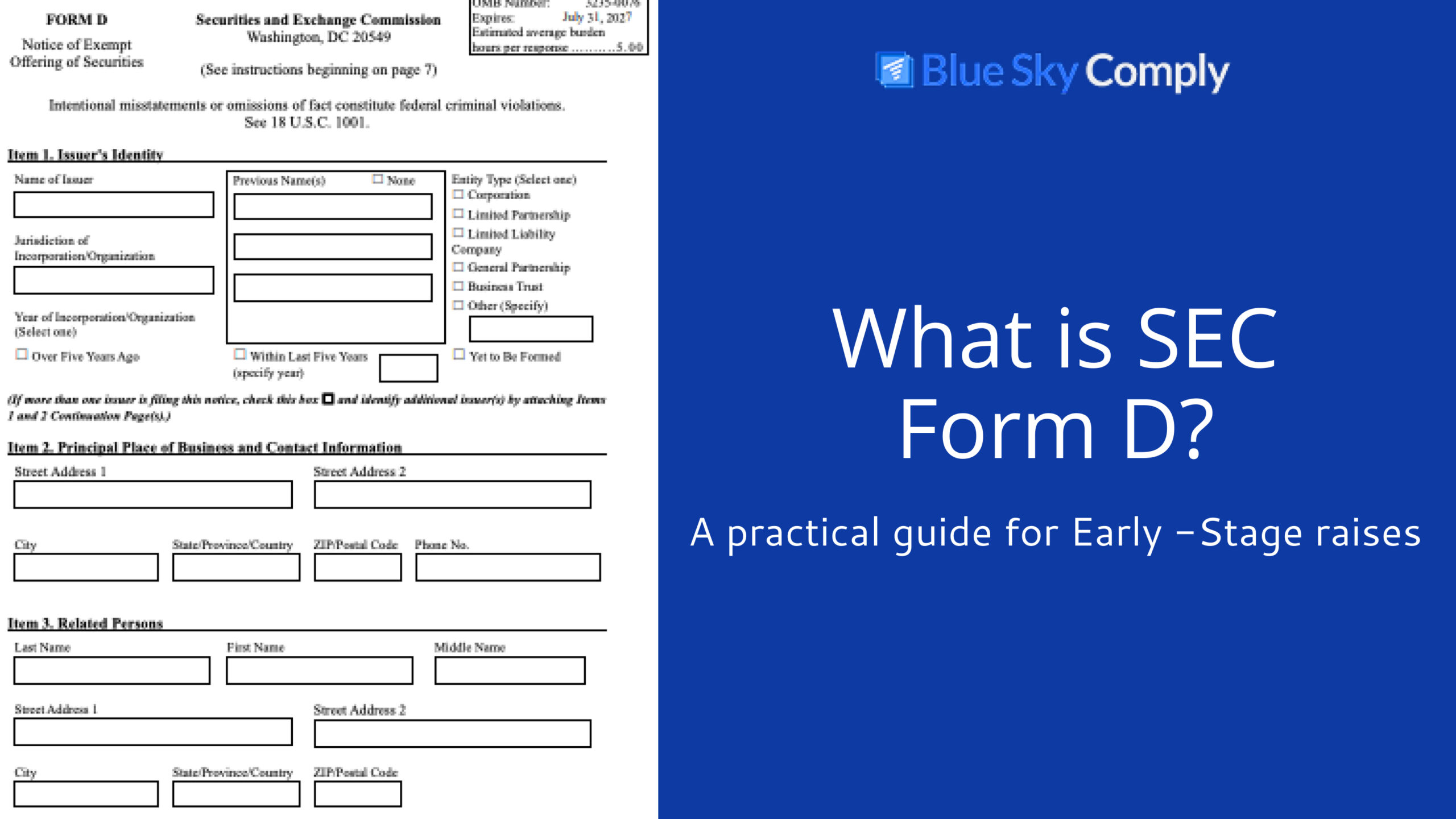

What Is SEC Form D?

SEC Form D is a notice filing submitted to the SEC for certain exempt offerings of securities, most commonly under Regulation D. It’s a concise disclosure about the issuer, the exemption relied upon, the size of the offering, sales to date, and basic information about investors and sales compensation. Form D is not a merit review or an approval process; it’s a formal notice that you are conducting a private offering under an exemption. Form D is typically associated with:- Rule 506(b) and 506(c) offerings

- Rule 504 offerings (smaller raises with burdensome filing requirements)

Who Must File Form D and When?

Issuers relying on Regulation D generally must file Form D with the SEC. This includes U.S. and foreign issuers selling securities in the United States. The filing deadline is within 15 calendar days after the “date of first sale.” Practically, the “first sale” occurs when an investor becomes irrevocably committed to invest, often when the subscription documents are signed, and funds are not subject to a unilateral right of withdrawal. A few operational points matter:- You need an EDGAR account, which can be obtained through a Form ID filing. That means your company (or the issuing vehicle) needs a CIK number and EDGAR filing codes before submitting. Getting these in place early avoids a deadline crunch.

- The deadline is short. Fifteen calendar days can pass quickly if you close over an SEC federal holiday or don’t have process ownership assigned.

What Information Does Form D Require?

Form D collects high-level offering and issuer details. Expect to provide:- Issuer identity and principal place of business, plus related persons (executive officers, directors, promoters).

- The exemption relied upon (e.g., 506(b), 506(c), or 504).

- Offering size: total amount, amount sold, minimum investment accepted.

- Investor mix: number of investors, and how many are accredited versus non-accredited (if applicable for your exemption).

- Sales compensation: whether you are paying placement agents, brokers, or finders, including names and CRD numbers where relevant.

- Offering jurisdictions: the states (and sometimes territories) where securities are being offered or sold.

How to File Form D on EDGAR (Step-by-Step)

The process is straightforward but benefits from preparation:- Obtain/confirm EDGAR credentials: Secure your CIK, CCC, and create appropriate filing roles in your system.

- Prepare the form: You can complete Form D directly on your blueskycomply.com account.

- Validate and submit: After completing the form with our validation checks and instructions providing guidance, you can submit a test filing to ensure you don’t have validation errors. You can then live file the document. If you prefer, we can handle all of this for you.

- Align the data: Make sure the data on your Form D matches your private placement memorandum, subscription documents, and investor list. Inconsistencies or inaccurate data could result in State or SEC fines.

Form D Amendments: When Are Updates Required?

You must amend Form D to correct material mistakes or reflect significant changes as the offering progresses. There’s also an annual amendment requirement if your offering is still ongoing on the first anniversary of the original filing. Common amendment triggers include:- A change in executive officers or directors

- A significant change in offering size or amount sold

- New sales compensation arrangements

- A change to issuer identity details or industry group - Additional selling jurisdictions that materially alter the picture

Blue Sky 101: State Notice Filings After Form D

Form D is federal. Most states still require notice filings and fees if you sell in their jurisdiction. While many states follow a similar structure, specifics vary—deadlines can be 15 days after the first sale in that state, and fee schedules can differ widely. States typically ask for multiple documents, including a copy of the Form D and payment of state fees. For multi-state raises, complexity ramps up quickly. You’re juggling deadlines, annual renewals, amendments, and changing requirements. If you’re getting oriented, our overview of the key requirements for Reg D offerings can help you understand where state notice filings fit into the broader compliance process.Common Mistakes and How to Avoid Them

Even seasoned teams can stumble on logistics. The most frequent issues include:- Missing the 15-day SEC deadline or state notice deadlines

- Starting the Form ID application process too late

- Inconsistencies between PPMs/sub docs, Form D, and state filings

- Forgetting to file or renew state notices in every jurisdiction where you’re selling

- Not amending Form D after material changes (or failing to update states accordingly)

- Overlooking disclosures about sales compensation or finders

Consequences of Non-Compliance

While a late or missing Form D won’t usually blow up your exemption by itself, it can create real problems. States may impose penalties, issue stop orders, assess additional late fees, or ask for corrective filings. You can heighten rescission risk if investors argue the offering wasn’t properly conducted, and you can create roadblocks during future diligence. **Non-compliance is costly, not just in fees, but also in lost time and possible legal trouble.**FAQs

- Do SPVs and funds need to file? Typically, yes, if relying on Reg D, the issuer (whether an SPV, fund, or operating company) is responsible for Form D and subsequent state notices.

- 506(b) vs. 506(c) vs. 504 506(b) doesn’t allow general solicitation and permits up to 35 non-accredited investors (with information requirements); 506(c) allows general solicitation but requires accredited investor verification; 504 is capped and subject to additional state considerations.

- If no sales occur, do you need to file? No first sale = no SEC Form D filing. But check any state-specific triggers if you conducted pre-filing activities or paid fees.

- How public is the information? EDGAR is public. Be thoughtful about what’s disclosed within the form’s structure and coordinate with counsel on investor optics.

Quick Comparison of Reg D Pathways

Before we jump into specifics, it helps to frame how the main Regulation D pathways differ in practice. Rule 506(b) is the traditional private placement; no general solicitation, with room for a limited number of non‑accredited investors if you provide robust disclosures. Rule 506(c) opens the door to public marketing, but only if every investor is verified as accredited. Rule 504 is typically used for smaller raises and involves more state‑level variation. The table below highlights the operational trade‑offs so you can choose the route that best fits your fundraising strategy.| Requirement | Rule 506(b) | Rule 506(c) | Rule 504 |

| General Solicitation | Not permitted | Permitted | Not permitted (with limited exceptions) |

| Investor Eligibility | Unlimited accredited; up to 35 non-accredited (with disclosures) | Accredited investors only (verification required) | Varies; generally open to non-accredited, subject to caps |

| Verification Requirement | Not required | Required (reasonable steps to verify) | Not required |

| Offering Cap | No SEC cap | No SEC cap | SEC cap applies (subject to change by rule) |

| Form D + State Notices | Yes + state notices as applicable | Yes + state notices as applicable | Yes + state notices as applicable, with more state variation |

Checklist: Getting Form D and Blue Sky Right

Pre-raise:- Secure your CIK and EDGAR codes.

- Confirm your exemption (e.g., 506(b) vs. 506(c)), align on investor eligibility and marketing plan.

- Draft PPM and other offering documents

- Calendar the 15-day SEC deadline and all state deadlines per jurisdiction.

- Ensure Form D data matches offering documents and internal records.

- Confirm EDGAR acceptance, save the filing receipt, and use it to support state Form D filings.

- Track amendments, renewals, and state responses until the offering is closed and all states are fully compliant.

How Blue Sky Comply Streamlines Form D and State Filings

Coordinating SEC and state filings for Reg D can be a full-time job, especially when your offering spans multiple closings, annual renewals, or several jurisdictions. Blue Sky Comply centralizes the data and timelines so you don’t have to chase scattered spreadsheets or emails.- Centralized workflow: We maintain a single source of truth for offering details, jurisdictions, deadlines, and fee schedules, and mirror these across federal and state requirements.

- Deadline and amendment tracking: Automated reminders help ensure your annual amendments and state renewals aren’t missed.

- Full-service support: From aligning sale dates and investor data with filings, our team supports counsel, funds, SPVs, and operating companies. For a deeper dive on the Reg D landscape, see our overview of a Reg D offering.

- Cost clarity: If you’re figuring out costs, our breakdown of Reg D State fees can help avoid surprises.

Getting the SEC Form D filing right isn’t about memorizing acronyms; it’s about entering the simple components to conducting a Reg D private offering.

In this article, we provide a field-by-field walkthrough that is designed for company executives/founders, CFOs, in-house counsel, and fund managers who want practical “how to complete Form D” guidance without the sales fluff. We’ll cover what you need before you start, how to move through each section with confidence, and the timing rules that trip teams up.

Form D is brief by SEC standards, but it touches on all critical points of your offering. Small inconsistencies can cascade into state-level issues later, such as:

- The wrong industry

- Investor count totals and amount sold discrepancies

- Incomplete related persons

- Inadequate commissions and finder's fees disclosures

- Proper Use of Proceeds disclosure.

What Form D Is, and When It’s Required

Form D is a notice filing with the SEC for certain private offerings. It makes basic details public: issuer identity, exemption claimed, offering size, and limited sales data. If you’re raising under the Regulation D framework, you should file within 15 days of the first sale. For a refresher on the exemption details and requirements, see Regulation D. Because Form D is public, coordinate your investor messaging and website language. You don’t need to over-share in the form, but everything must be accurate, consistent, and timely across federal and state submissions.How Companies Use Form D in Practice

Real-world filings make the mechanics tangible. The companies below illustrate common Form D patterns you will likely encounter, including rolling closes that require timely amendments, disciplined tracking of investor counts and jurisdictions, and tight alignment between issuer identity, related persons, and any sales compensation. Use these as mental models to pressure test your own process before and after each close.- SpaceX: Amending as Large Rounds Progress: SpaceX has filed multiple Form Ds across successive equity rounds. As funds accumulate through rolling closes, filings reflect updated “amount sold” and added jurisdictions. The practical takeaway: for staged capital collection, build a rhythm of checking amendment triggers after each close so federal and state records stay aligned.

- Stripe: Rolling Closes and Timing Discipline: Stripe’s Form D history illustrates how high-demand raises can proceed in increments. Investor counts and amounts sold change as allocations settle, driving timely amendments. The takeaway: pair your closing calendar with a 48-hour “amend-or-not” review to keep the public record current.

- Epic Games: Clean Issuer Identity and Compensation Alignment: Epic Games filings are a straightforward model for issuer identity, related persons, and sales compensation entries. The takeaway: match titles to your board resolutions, and ensure any cash, warrants, or success-fee equity given for placement activity is consistently reflected across agreements, the cap table, and Form D.

- Early-Stage Startups: First-Sale Date and Jurisdiction Nuance: Many seed and Series A companies trigger their first-sale date when the first wire lands under executed subscription agreements, not when soft commits arrive. The takeaway: track investor legal residence at subscription, not after funds clear; that’s what drives state notice filings and related fees.

Potential Pitfalls of the Form D (and Form ID)

Before you can file Form D, you need EDGAR access. That starts with Form ID—your application to obtain or update EDGAR credentials (CIK/CCC and related access). Since EDGAR Next changes, the SEC has frequently taken several days to approve new Form ID submissions, which can push your Form D timing if you wait until the last minute. Build this lag into your deal calendar and kick off Form ID well before first close.Why Form ID matters

- Form ID is the gatekeeper. Without it, you can’t file Form D. Approvals often take several days post–EDGAR Next, especially for first-time issuers and new signers.

- Notarized signatures are required. Plan for a notarized, correctly executed signature page. We can help coordinate notarization and submission so the package is accepted the first time.

- Waiting until the week of first close: Start Form ID 2–3 weeks before your expected first sale date. Have a backup signatory ready with a notarized page in case your primary signer is unavailable.

- Signature/notary defects: Name/title mismatch with corporate records, missing notary seal, or date issues are common rejection reasons. Align titles with board resolutions and ensure the notary block is complete and legible.

- Identity and document mismatches: The legal name on Form ID must match formation documents exactly. Avoid using DBAs. If you’re updating credentials for a new executive signer, align with your Related Persons details.

- File format and submission errors: Follow the SEC’s file type and size specs. Incorrect PDFs or corrupt attachments can trigger rejections and restart the clock.

- Role confusion: Don’t use a personal EDGAR account to file for the issuer. Establish issuer credentials and assign the proper roles so the authorized officer can sign Form D.

- Contact details that don’t resolve: Use monitored email and phone numbers; SEC confirmations and queries arrive via those channels, and timing matters.

Before You Start: Prerequisites and Setup

Before you dive into the form, set your foundation. Decide which exemption actually matches how you marketed the raise, secure EDGAR access by submitting Form ID early (approvals can take several days after EDGAR Next and require a notarized signature), assign clear internal owners for data, and pull a single, current set of records for issuer details, officers, industry/NAICS, offering terms, investor counts, jurisdictions, and any sales compensation. With that groundwork in place, you’ll file faster and avoid amendment churn. Here are the prerequisites:Confirm Your Exemption and Offering Structure

Most private issuers rely on Rule 506(b) or 506(c). The key differences affect both how you market and what you must validate for investors.- 506(b) prohibits general solicitation but allows up to 35 non-accredited investors (with disclosure requirements).

- 506(c) permits general solicitation if you take reasonable steps to verify accredited status.

- Scenario 1: You posted your deck publicly after a conference. That’s general solicitation, use 506(c), and verify accreditation before accepting funds.

- Scenario 2: You quietly raised from a known network with no public marketing. 506(b) may fit—track any non-accredited investors and deliver required disclosures.

Get Your EDGAR Credentials in Order

First, file Form D through EDGAR. Make sure you have:- CIK, CCC, and related EDGAR access codes

- Authorized personnel identified (and available on filing day)

- A secure process for sharing credentials

Gather Required Information (Working Checklist)

Form D pulls from multiple systems, including legal, finance, HR, and investor relations. Centralize:- Issuer details (legal name, entity type, jurisdiction, addresses, EIN, year of incorporation)

- Related persons (executive officers, directors, promoters; names, titles)

- Industry

- Issuer size and revenue range

- Exemption claimed (e.g., Rule 506(b), 506(c), 504)

- Offering details (total offering amount, minimum investment, date of first sale)

- Sales data (amount sold, number of investors; accredited vs. non-accredited where applicable)

- Sales compensation (agents, brokers, finders, and associated fees)

- Use of proceeds

- Jurisdictions of sales (this drives state notice filings)

- Authorized signatory for submission

The Form D Instructions: Field-by-Field Guide

Before you open EDGAR, pull up your latest corporate records, board resolutions, subscription trackers, and cap table. This field-by-field guide explains what each Form D item is asking for, how to enter it correctly the first time, and which details commonly trigger corrections. Keep names, titles, NAICS, offering amounts, investor counts, jurisdictions, and any sales compensation aligned to the same single source of truth; when facts change during rolling closes, amend promptly so your federal and state records stay in sync.- Issuer Information: Enter the issuer’s full legal name exactly as it appears in formation documents. Specify the entity type and jurisdiction of incorporation/organization. The primary business address should reflect where the company operates; the mailing address can differ. Include your EIN if requested. This section sets the identity anchor for everything else. Mismatches here can ripple into state systems.

- Related Persons (Executive Officers, Directors, Promoters): List each relevant individual with full name and title. Title accuracy matters; use official titles that match your corporate records and any prior disclosures. If leadership changes during the raise, you may trigger an amendment to keep Form D current.

- Industry Group and NAICS: Pick the most accurate industry possible that aligns with your NAICS code. Don’t guess. Cross-check with your tax and payroll records. When in doubt, select the industry that best reflects primary revenue generation, not a future roadmap. A mismatched industry can cause follow-up questions from states and investors.

- Revenue Range and Size of Issuer: Choose the category that best reflects your most recent fiscal-year figures or current state, per the form’s instructions. Be consistent with what you disclose elsewhere (offering materials, investor communications, and state filings). Note that you can decline to disclose.

- Exemption/Exclusion Claimed: Select Rule 506(b) or 506(c) based on your actual marketing and verification practices (we recommend avoiding Rule 504). If you generally solicit, 506(c) is the typical path, and you must verify accredited status. If you didn’t solicit, 506(b) is common, with limits and disclosure obligations for any non-accredited investors. This field influences what you must track and how states may review your filing.

- Offering Details: Report the total offering amount (even if you don’t intend to sell every dollar immediately). If the amount is open-ended, follow the form’s “indeterminate” conventions. Enter the amount sold to date, the minimum investment (if any), and the date of first sale. This date starts your federal and state due date requirements of filings being done within 15 days of the first sale.

- Sales Commissions and Finder’s Fees: Disclose compensation to placement agents, broker-dealers, finders or anyone receiving sales commission of any kind, including amounts or ranges. Identify the recipients where required. If you have success fees or warrants for intermediaries, ensure they’re reflected accurately. Underreporting here is a common audit and regulator sore spot.

- Use of Proceeds: Describe the general categories, working capital, product development, acquisitions, debt repayment, etc. Keep it aligned with your offering materials. If any proceeds compensate executive officers or directors, follow the form’s instructions on disclosure.

- Investor and Sales Data: Enter the number of investors admitted to date. For 506(b) offerings, the count of non-accredited investors (if any) must be tracked with care. For 506(c), ensure your accreditation verification records are in order, even if you don’t upload them here. If you’re doing rolling closes, you may need to amend investor counts and amounts sold as the raise progresses.

- Jurisdictions: If you are paying commissions (from above), please list the states (and, if applicable, territories) where sales occurred. This section is pivotal for your state notice filings. Many states require notice filings and fees shortly after the first sale in that state, independent of the SEC clock.

- Signatures and Submission: Form D should be signed by an authorized person, typically an executive officer. Double-check name/title alignment with the Related Persons section. Once filed, EDGAR will time-stamp the submission and make it publicly accessible.

Form D Deadlines: Initial Filing, Amendments, and Closing Out

Your initial Form D is due within 15 calendar days after the date of first sale, which generally means the date you have a binding investment commitment and receive consideration (or are irrevocably committed to receive it). If your first sale happens on a weekend or holiday, count forward; the 15-day clock doesn’t pause. You must amend Form D for certain material changes, such as:- A significant change in the offering amount or the amount sold

- A change in the exemption claimed (e.g., switching 506(b) to 506(c))

- Changes to issuer identity details or related persons

- New jurisdictions where sales occur

- Other possible changes that we can guide you through at Blue Sky Comply.

After You File: State Notice Filings and Fees

Filing Form D federally doesn’t complete your compliance. Most states require their own notice filings and fees when you sell to investors in that state, often tied to the first sale date in that jurisdiction. The data you enter on Form D (issuer details, exemption, offering size, sales) should match what you submit to the states. Inconsistency can create back-and-forth and late fees. If you’re budgeting your raise, scan typical costs with Reg D state fees and plan submissions by jurisdiction. For the broader landscape of what states expect, see state securities filings. Keeping a single source of truth for amounts sold, investor counts, and dates will make multi-state maintenance much smoother.FAQ: Practical Questions About Form D Instructions

- Do I need a Form D before accepting soft commitments? No. The Form D can be filed after the first sale, when the investor has signed the purchase or subscription agreement, the clock is typically started.

- Can I pre-file the Form D to the SEC and States before I make any sales? Yes, you can pre-file to the SEC before making any sales, and to the states as well to ensure you are cleared and ready in advance.

- Do I have to do a Renewal filing after 1 year to keep my offering open? Yes, you have to file a Form D renewal filing each year before the 12-month mark. State filings may be required depending on the state, which we can help with.

- What if my offering amount changes mid-raise? If the total offering amount shifts materially, amend the Form D and align state notices. Keep your offering documents synchronized.

- How public is my Form D? Very. It’s accessible on the SEC EDGAR Search. Plan investor communications and PR with that visibility in mind.

Bottom Line

Form D is straightforward when you prepare your inputs and keep your records reconciled. The flow is simple: assemble clean issuer and offering data, complete the fields carefully, file on time, amend when facts change, and finish strong with state notices. Your raise moves faster when your filings tell a single, consistent story. And, lastly, don’t forget annual renewal obligations. Blue Sky Comply can help you with Form D filings and Reg D blue Sky filings.

Filing Form D is a critical step for many companies raising capital under Regulation D of the Securities Act of 1933. While Regulation D private offerings allow businesses to raise money without registering their securities with the SEC, Form D acts as a required notice of the exempt offering and must be filed electronically through the SEC’s EDGAR system.

This article explains who is required to file Form D, when it must be filed, and what it includes.

What Is Form D?

Form D is a brief notice filed with the SEC to claim an exemption from full registration under Regulation D. It includes basic information about the issuer, the type and amount of securities offered, and the identity of certain individuals involved in the offering. Importantly, Form D is not an application for exemption approval—it is a notification that the issuer is relying on one of the exemptions under Regulation D.What Entities Are Required to File Form D?

The following parties are required to file Form D with the SEC:Companies Offering Securities Under Rule 504

- Can raise up to $10 million in a 12-month period.

- No federal preemption: issuers must also comply with state-level Blue Sky registration or exemption requirements.

- Form D is required to notify the SEC of the exempt offering.

Companies Offering Securities Under Rule 506(b)

- Can raise an unlimited amount of capital.

- Can sell to an unlimited number of accredited investors and up to 35 non-accredited (but sophisticated) investors.

- Offers are not publicly advertised.

- Federal preemption applies, but Form D is still required as a notification filing.

Companies Offering Securities Under Rule 506(c)

- Allows general solicitation and advertising of the offering.

- All investors must be accredited and verified.

- No limit on the amount of capital raised.

- Like 506(b), Form D is required and federal preemption applies, though state notice filings are still mandatory in most jurisdictions.

Any Domestic or Foreign Private Issuer Using a Reg D Exemption

- Whether a U.S. company or a foreign issuer, if they are offering securities under Reg D to U.S. investors, Form D must be filed with the SEC.

Investment Funds and Private Equity Firms

- Hedge funds, venture capital funds, and private equity firms frequently rely on Rule 506 exemptions and are required to file Form D when raising capital from investors.

Startups and Early-Stage Companies

- Most early-stage companies raising capital through friends, family, angel investors, or venture capital under Reg D are legally obligated to file Form D with the SEC to remain in compliance.

When Must Form D Be Filed?

Form D must be filed within 15 calendar days after the first sale of securities in the offering.- A “sale” occurs when an investor is legally obligated to invest, not necessarily when funds are received.

- If the 15th day falls on a weekend or federal holiday, the deadline is extended to the next business day.

What Happens If You Don’t File Form D?

- Loss of exemption: Issuers that fail to file Form D may lose their Reg D exemption and be forced to register the offering or return investor funds.

- State enforcement: Many states also require notice filings that depend on timely SEC Form D submission.

- Reputational risk: Noncompliance can harm investor confidence and damage relationships with future backers or partners.

- Future fundraising limitations: Issuers may be barred from relying on Regulation D for future offerings.

What’s Included in Form D?

- Basic company information (name, address, jurisdiction)

- Offering size and amount already sold

- Type of security being offered

- Minimum investment accepted

- Use of proceeds

- Details about executive officers, promoters, and related parties

- Exemption rule being relied upon (504, 506(b), or 506(c))

Best Practices

- Track offering dates and file Form D before the 15-day deadline

- Coordinate state Blue Sky notice filings alongside your federal Form D

- Work with a compliance professional to ensure accuracy and timely filing

- Amend Form D if material information changes (e.g., increase in offering size)

Conclusion

Any company raising capital under Regulation D Rules 504, 506(b), or 506(c) must file Form D with the SEC. Filing is mandatory, not optional—even if you're a private company, foreign issuer, or raising from accredited investors only. Need Help? Blue Sky Comply offers turnkey support for Form D preparation, SEC submission, and state-level Blue Sky filings to help you stay compliant and focused on raising capital.

Navigating federal securities law is complex—but it becomes even more challenging when layered with individual state securities regulations, known as Blue Sky laws. While certain SEC filings benefit from federal preemption, many still trigger state-level notice, exemption, or registration requirements. Skipping these steps can result in costly fines, cease and desist orders, or enforcement actions.

What Are Blue Sky Filings?

Blue Sky laws are state-level securities laws designed to protect investors from fraud. Even if an offering is exempt from federal registration, the issuer often must submit a notice filing with each state where the securities are offered or sold. These filings frequently include a copy of the SEC form (such as Form D), a consent to service of process (typically Form U-2), and a filing fee.SEC Filings That Trigger Blue Sky Filings

Below is a detailed breakdown of the most common SEC filings and how they interact with Blue Sky law obligations at the state level.Form D (Regulation D: Rules 504, 506(b), 506(c))

- Triggers Blue Sky filings in all states where securities are sold.

- Rule 504: No federal preemption. Issuers must register or file for exemption in each state.

- Rules 506(b) and 506(c): Federal preemption applies under the National Securities Markets Improvement Act (NSMIA), but issuers must still file notice filings and fees with each applicable state.

Form 1-A (Regulation A: Tier 1 and Tier 2 Offerings)

- Tier 1 (up to $20M): No federal preemption. Full Blue Sky registration is required in every state where securities are offered.

- Tier 2 (up to $75M): Federal preemption of registration, but most states still require notice filings and fees, including Form 1-A, U-2, and filing fees.

- Some states require issuer-dealer registration for direct sales to investors.

Form C (Regulation Crowdfunding - Reg CF)

Although Reg CF enjoys federal preemption, some states still require a Blue Sky notice filing for crowdfunding offerings. Required filings often include:- A notice filing of the Reg CF offering

- A filing fee

- Any applicable state-specific forms

- Investor Residency Concentration: Individuals who purchase 50% or more of the total securities sold (via dollar amount) in the Reg CF offering are residents of the corresponding state.

- State of Principal Place of Business: If your principal place of business is located in a U.S. State that mandates state filings, you may need to comply with these requirements.

Form S-1 (Initial Public Offerings and Direct Listings)

- Used for public offerings of securities.

- If securities are not listed on a national securities exchange (like NASDAQ or NYSE), Blue Sky registration may be required in states where the securities are sold.

- Some states require issuer-dealer or agent registration for direct-to-investor IPOs.

Forms S-3, S-4, S-8, F-1, F-3, F-4

- Used for follow-on offerings, mergers, employee stock compensation, and foreign issuer registrations.

- If securities are NMS-listed (traded on a national securities exchange), Blue Sky laws are typically preempted.

- However, resale of securities or direct offerings to employees (e.g., via S-8) may still trigger notice filings in specific states.

Form 10 / Form 8-A

These forms are used for registering securities under the Securities Exchange Act of 1934.- If the issuer’s securities are not listed on a national exchange, Blue Sky registration or exemption may still be required for secondary sales in some states.

Rule 147 / Rule 147A (Intrastate Offerings)

- These rules allow for intrastate offerings exempt from federal registration.

- Issuers must comply fully with the Blue Sky registration or exemption process in the offering state.

Regulation S (Offshore Offerings)

- Reg S allows offerings made outside the U.S. to foreign investors.

- Generally does not require Blue Sky filings, unless securities are later resold in U.S. states. In such cases, state-level compliance may be required for secondary market activity.

Rule 701 (Employee Compensation Plans for Private Companies)

- Allows companies to issue equity as compensation to employees without federal registration.

- Several states require a Blue Sky notice filing if employees reside in their jurisdiction and receive equity under Rule 701.

Regulation E (Closed-End Investment Companies)

- Applies to small business investment companies or BDCs (business development companies).

- Triggers Blue Sky filings in each state where securities are sold.

Regulation CE (Rule 1001 – California-Only Exemption)

- Applies only to California-based offerings under federal exemption.

- Still requires compliance with California Blue Sky laws.

What Happens If You Don’t File?

Failure to comply with Blue Sky laws may result in:- Fines from $100 to $5,000+ per violation

- Cease and desist orders

- Rescission rights for investors

- Barred ability to raise capital in noncompliant states

- Reputational harm

Best Practices for Issuers

- Determine investor locations early in the offering process

- Track and meet all filing deadlines (e.g., 15-day window post-sale for Form D)

- Budget for state fees (ranging from $100 to over $2,500 per state)

- Use an experienced Blue Sky compliance partner to ensure filings are timely, complete, and cost-effective

Need Help?

At Blue Sky Comply, we monitor all 50 states and D.C. for compliance rules, filing requirements, and deadlines. Whether you're raising under Reg D, Reg A, Reg CF, or another exemption or offering, we provide expert filing services and cost-saving compliance management.

Ensuring compliance with Blue Sky Laws is essential for any issuer conducting a securities offering. These state-level regulations govern the sale of securities and protect investors from fraudulent activities. Companies must navigate complex filing requirements, including initial notice filings, annual renewals, and amendments when necessary. Failing to comply with these rules can lead to fines, restrictions on securities sales, and legal penalties.

This guide explores how often issuers should file Blue Sky filings, outlining the key requirements for different types of securities offerings and best practices for maintaining compliance.

What Are Blue Sky Filings?

Blue Sky filings are state-mandated regulatory filings required for securities offerings. These filings notify state regulators of securities transactions and ensure compliance with state securities laws. The frequency of Blue Sky filings depends on several factors, including the type of securities offering, state-specific requirements, and whether the issuer is conducting a public or private placement. Understanding these requirements is crucial for issuers to avoid penalties and maintain good standing in each jurisdiction where they offer securities.Initial Notice Filings

For most exempt securities offerings, issuers must file an initial notice with each state where securities are sold.- Regulation D Offerings (Rule 506(b) and 506(c)) require issuers to submit a Form D notice filing to the SEC within 15 days of the first sale of securities. Many states also require a corresponding Blue Sky notice filing within the same period.

- Regulation A Tier 1 Offerings require issuers to complete full state registration before they can offer securities, meaning filings must be submitted before any securities are sold.

- Regulation A Tier 2 Offerings benefit from state law preemption but still require notice filings in certain states. These filings must typically be submitted within 15 days of the first sale.

Annual Renewal Filings

Many states require issuers to renew their Blue Sky filings annually to continue selling securities within their jurisdiction.- Regulation A Tier 1 issuers must complete annual renewals in each state where securities are registered.

- Regulation D Offerings may require renewals in certain states if the offering is ongoing beyond the initial year.

- Some states, such as Colorado and Nevada, impose annual renewal requirements to maintain compliance.

Amendment Filings

In addition to initial and renewal filings, issuers must file amendments if there are significant changes to the offering. Amendments may be required when:- The total amount of securities offered changes.

- There are modifications to the issuer’s executive officers or directors.

- The terms and conditions of the securities being sold are altered.

- The offering extends beyond the initially expected timeframe.

Ongoing Compliance Requirements

Beyond initial, renewal, and amendment filings, issuers must track their obligations in multiple states to ensure full compliance.- Some states require quarterly or semi-annual reports for certain offerings, particularly under Regulation A.

- Ongoing reporting requirements may include financial disclosures and investor updates to ensure continued transparency.

- Failure to comply with these obligations can lead to penalties, regulatory scrutiny, and the potential revocation of the issuer’s ability to sell securities in a state.

Best Practices for Managing Blue Sky Filings

To stay compliant with Blue Sky Laws, issuers should implement best practices for tracking and managing filing deadlines:- Develop a compliance calendar to track filing due dates, renewal deadlines, and amendment requirements.

- Monitor state-specific filing changes, as regulations may vary and evolve over time.

- Work with compliance professionals who specialize in Blue Sky filings to streamline the process and reduce the risk of errors.

- Maintain accurate records of all filings and communications with state regulators to demonstrate compliance if audited.

The Consequences of Non-Compliance

Failure to adhere to Blue Sky filing requirements can have significant consequences, including:- State-imposed fines and penalties, which can range from $500 to $10,000 per violation.

- Restrictions on offering securities in states where filings are delinquent or incomplete.

- Legal actions from state regulators that may impact future fundraising efforts.

- Loss of investor confidence, as non-compliance can raise red flags for potential stakeholders.

Conclusion

Ensuring Compliance with Blue Sky Filings Staying compliant with Blue Sky Laws requires issuers to stay on top of filing deadlines, renewal obligations, and amendment requirements. Whether conducting a Regulation D, Regulation A, or other exempt securities offering, issuers must ensure they meet all state-level filing obligations to avoid penalties and maintain the ability to raise capital.

Let Us Simplify Compliance for You

Partner with Blue Sky Comply to unlock seamless compliance, efficient filings, and access to expertise that lets you focus on your growth.

Schedule A Free Demo