If you’re raising private capital in the U.S., there’s a good chance you’re relying on Regulation D. That’s where SEC Form D comes in, a short notice filing for private offerings conducted by any companies in the United States – yes, this means all companies in the US who sell securities to investors must file a Form D to the SEC with the accompanying Blue Sky filings.

The SEC Form D doesn’t get you “approval,” but it does provide basic disclosure of key details of your exempt offering and starts the 15-day filing window for your state-level “blue sky” obligations. In other words, it’s a notice form with consequences for compliance, investor confidence, and your fundraising momentum.

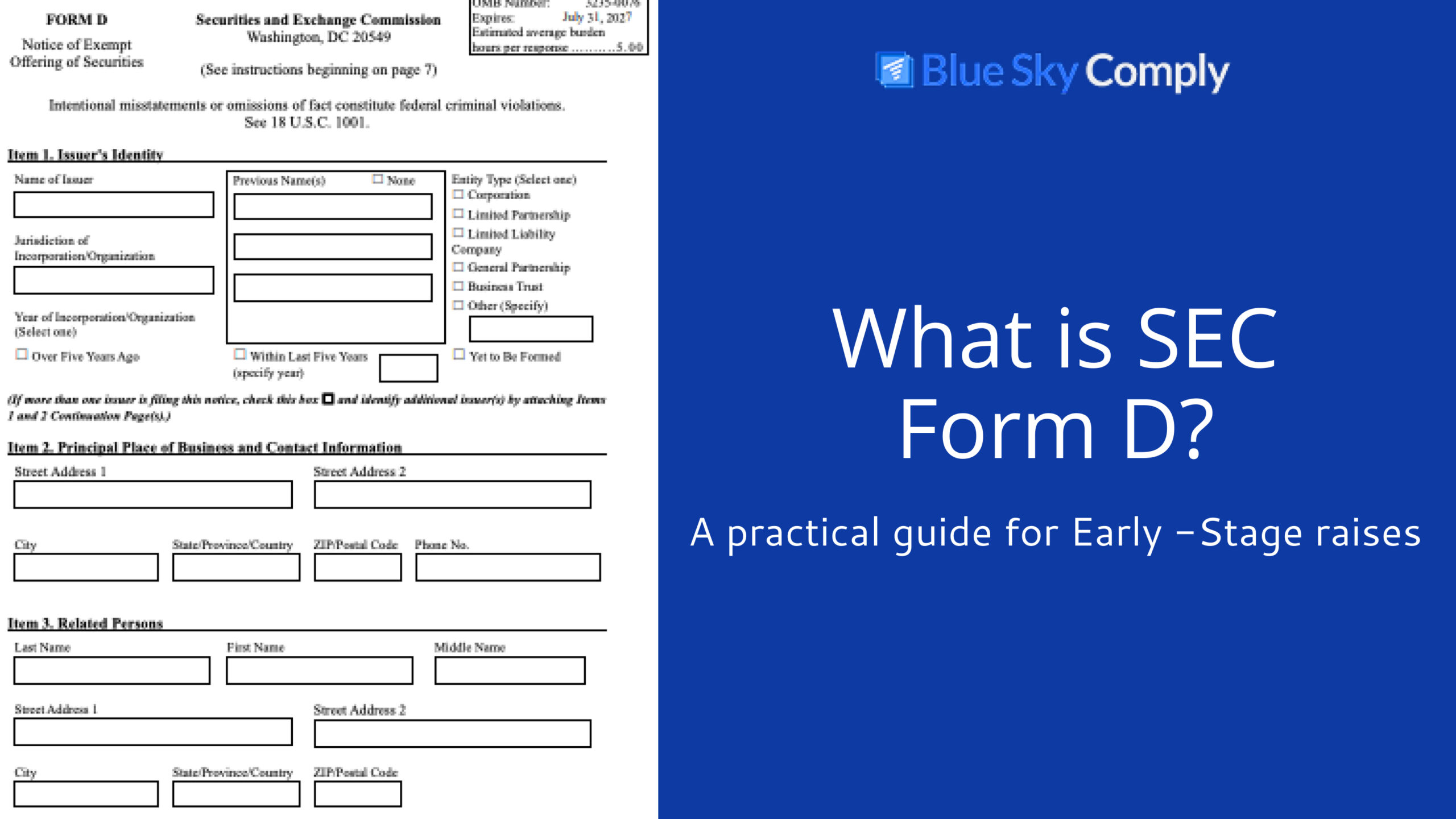

What Is SEC Form D?

SEC Form D is a notice filing submitted to the SEC for certain exempt offerings of securities, most commonly under Regulation D. It’s a concise disclosure about the issuer, the exemption relied upon, the size of the offering, sales to date, and basic information about investors and sales compensation. Form D is not a merit review or an approval process; it’s a formal notice that you are conducting a private offering under an exemption.

Form D is typically associated with:

- Rule 506(b) and 506(c) offerings

- Rule 504 offerings (smaller raises with burdensome filing requirements)

If you’re using other exemptions, your filing may be different (e.g., Regulation Crowdfunding uses Form C; Regulation A uses Form 1-A). But for most private placements, Form D is the gold standard.

Who Must File Form D and When?

Issuers relying on Regulation D generally must file Form D with the SEC. This includes U.S. and foreign issuers selling securities in the United States. The filing deadline is within 15 calendar days after the “date of first sale.” Practically, the “first sale” occurs when an investor becomes irrevocably committed to invest, often when the subscription documents are signed, and funds are not subject to a unilateral right of withdrawal.

A few operational points matter:

- You need an EDGAR account, which can be obtained through a Form ID filing. That means your company (or the issuing vehicle) needs a CIK number and EDGAR filing codes before submitting. Getting these in place early avoids a deadline crunch.

- The deadline is short. Fifteen calendar days can pass quickly if you close over an SEC federal holiday or don’t have process ownership assigned.

What Information Does Form D Require?

Form D collects high-level offering and issuer details. Expect to provide:

- Issuer identity and principal place of business, plus related persons (executive officers, directors, promoters).

- The exemption relied upon (e.g., 506(b), 506(c), or 504).

- Offering size: total amount, amount sold, minimum investment accepted.

- Investor mix: number of investors, and how many are accredited versus non-accredited (if applicable for your exemption).

- Sales compensation: whether you are paying placement agents, brokers, or finders, including names and CRD numbers where relevant.

- Offering jurisdictions: the states (and sometimes territories) where securities are being offered or sold.

Because Form D is public on EDGAR, many issuers coordinate closely with counsel to ensure the disclosures are accurate, consistent with offering documents and the private placement memorandum (PPM), and reflect an appropriate level of detail.

How to File Form D on EDGAR (Step-by-Step)

The process is straightforward but benefits from preparation:

- Obtain/confirm EDGAR credentials: Secure your CIK, CCC, and create appropriate filing roles in your system.

- Prepare the form: You can complete Form D directly on your blueskycomply.com account.

- Validate and submit: After completing the form with our validation checks and instructions providing guidance, you can submit a test filing to ensure you don’t have validation errors. You can then live file the document. If you prefer, we can handle all of this for you.

- Align the data: Make sure the data on your Form D matches your private placement memorandum, subscription documents, and investor list. Inconsistencies or inaccurate data could result in State or SEC fines.

Form D Amendments: When Are Updates Required?

You must amend Form D to correct material mistakes or reflect significant changes as the offering progresses. There’s also an annual amendment requirement if your offering is still ongoing on the first anniversary of the original filing. Common amendment triggers include:

- A change in executive officers or directors

- A significant change in offering size or amount sold

- New sales compensation arrangements

- A change to issuer identity details or industry group – Additional selling jurisdictions that materially alter the picture

As a practical rule, file amendments “as soon as practicable” after the change, and keep your state filings harmonized with the federal data.

Blue Sky 101: State Notice Filings After Form D

Form D is federal. Most states still require notice filings and fees if you sell in their jurisdiction. While many states follow a similar structure, specifics vary—deadlines can be 15 days after the first sale in that state, and fee schedules can differ widely. States typically ask for multiple documents, including a copy of the Form D and payment of state fees.

For multi-state raises, complexity ramps up quickly. You’re juggling deadlines, annual renewals, amendments, and changing requirements. If you’re getting oriented, our overview of the key requirements for Reg D offerings can help you understand where state notice filings fit into the broader compliance process.

Common Mistakes and How to Avoid Them

Even seasoned teams can stumble on logistics. The most frequent issues include:

- Missing the 15-day SEC deadline or state notice deadlines

- Starting the Form ID application process too late

- Inconsistencies between PPMs/sub docs, Form D, and state filings

- Forgetting to file or renew state notices in every jurisdiction where you’re selling

- Not amending Form D after material changes (or failing to update states accordingly)

- Overlooking disclosures about sales compensation or finders

Two practical safeguards go a long way: assign a clear owner for Form D and state filings, and maintain a single, constantly updated spreadsheet or system capturing offering details, investors, jurisdictions, and fees. Regulators care about timeliness and accuracy; clean, consistent records reduce risk and friction.

Consequences of Non-Compliance

While a late or missing Form D won’t usually blow up your exemption by itself, it can create real problems. States may impose penalties, issue stop orders, assess additional late fees, or ask for corrective filings. You can heighten rescission risk if investors argue the offering wasn’t properly conducted, and you can create roadblocks during future diligence. **Non-compliance is costly, not just in fees, but also in lost time and possible legal trouble.**

FAQs

- Do SPVs and funds need to file?

Typically, yes, if relying on Reg D, the issuer (whether an SPV, fund, or operating company) is responsible for Form D and subsequent state notices. - 506(b) vs. 506(c) vs. 504

506(b) doesn’t allow general solicitation and permits up to 35 non-accredited investors (with information requirements); 506(c) allows general solicitation but requires accredited investor verification; 504 is capped and subject to additional state considerations. - If no sales occur, do you need to file?

No first sale = no SEC Form D filing. But check any state-specific triggers if you conducted pre-filing activities or paid fees. - How public is the information?

EDGAR is public. Be thoughtful about what’s disclosed within the form’s structure and coordinate with counsel on investor optics.

Quick Comparison of Reg D Pathways

Before we jump into specifics, it helps to frame how the main Regulation D pathways differ in practice. Rule 506(b) is the traditional private placement; no general solicitation, with room for a limited number of non‑accredited investors if you provide robust disclosures. Rule 506(c) opens the door to public marketing, but only if every investor is verified as accredited. Rule 504 is typically used for smaller raises and involves more state‑level variation. The table below highlights the operational trade‑offs so you can choose the route that best fits your fundraising strategy.

| Requirement | Rule 506(b) | Rule 506(c) | Rule 504 |

| General Solicitation | Not permitted | Permitted | Not permitted (with limited exceptions) |

| Investor Eligibility | Unlimited accredited; up to 35 non-accredited (with disclosures) | Accredited investors only (verification required) | Varies; generally open to non-accredited, subject to caps |

| Verification Requirement | Not required | Required (reasonable steps to verify) | Not required |

| Offering Cap | No SEC cap | No SEC cap | SEC cap applies (subject to change by rule) |

| Form D + State Notices | Yes + state notices as applicable | Yes + state notices as applicable | Yes + state notices as applicable, with more state variation |

Checklist: Getting Form D and Blue Sky Right

Pre-raise:

- Secure your CIK and EDGAR codes.

- Confirm your exemption (e.g., 506(b) vs. 506(c)), align on investor eligibility and marketing plan.

- Draft PPM and other offering documents

At first sale:

- Calendar the 15-day SEC deadline and all state deadlines per jurisdiction.

- Ensure Form D data matches offering documents and internal records.

After submission:

- Confirm EDGAR acceptance, save the filing receipt, and use it to support state Form D filings.

- Track amendments, renewals, and state responses until the offering is closed and all states are fully compliant.

How Blue Sky Comply Streamlines Form D and State Filings

Coordinating SEC and state filings for Reg D can be a full-time job, especially when your offering spans multiple closings, annual renewals, or several jurisdictions. Blue Sky Comply centralizes the data and timelines so you don’t have to chase scattered spreadsheets or emails.

- Centralized workflow: We maintain a single source of truth for offering details, jurisdictions, deadlines, and fee schedules, and mirror these across federal and state requirements.

- Deadline and amendment tracking: Automated reminders help ensure your annual amendments and state renewals aren’t missed.

- Full-service support: From aligning sale dates and investor data with filings, our team supports counsel, funds, SPVs, and operating companies. For a deeper dive on the Reg D landscape, see our overview of a Reg D offering.

- Cost clarity: If you’re figuring out costs, our breakdown of Reg D State fees can help avoid surprises.

For raises that touch other exemptions, check out our primers on a Reg A offering and Regulation CF to understand how the filings differ and how state requirements interact.

Note: we don’t provide legal advice, please consult your legal counsel with any questions.